Affordable Care Act

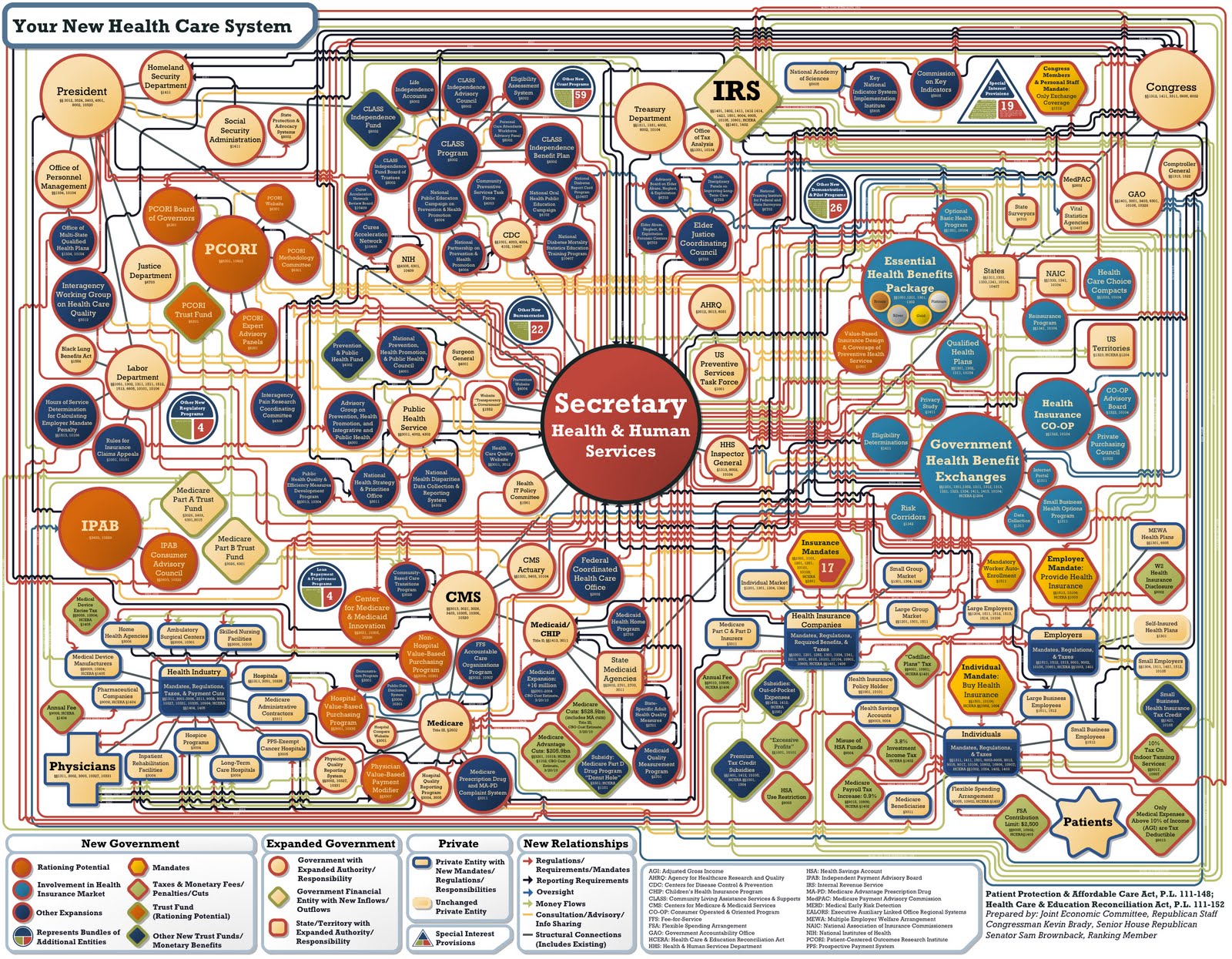

Healthcare Reform is a complicated issue. This diagram was prepared by the JointEconomic Committee, and shows just how much consideration had to go into developing a plan.

Fortunately, they made room for Physicians in the bottom left and Patients in the bottom right.That they’re not directly connected might be a slight oversight. There are four key provisions of the Patient Protection and Affordable Care Act, typically referred to as the ACA, that will affect most people: Exchanges, Subsidies, Guaranteed Insurability, and Individual Coverage Mandates.

Exchanges (also referred to as The Marketplace) are a place where people can go to compare health insurance plans and premiums. In Oregon, it’s called Cover Oregon, and in Washington, it’s called the Washington Healthplan Finder. As much as possible, it’s an apples-to-apples comparison. Carriers now have to design their plans based on Metal Tiers. You may see Platinum, Gold, Silver, and Bronze levels of benefits, although carriers aren’t required to offer benefits within every tier. And with some minor variation, a Gold Plan is a Gold Plan no matter which carrier you use. One critical issue now will be the Provider Network. This will be the easiest way for carriers to affect their rates. So expect carriers to tighten up their networks, and cut out expensive provider groups. The primary reason that one would use an Exchange rather than going directly to a carrier, is the subsidy.

Subsidies are determined by your Modified Adjusted Gross Income (MAGI). If your MAGI is below 400% of the poverty level, you may qualify for a subsidy. The subsidy can be used to reduce your premium, or as a tax credit when you file. There are subsidy calculators available on the websites for all of the Exchanges. There’s also an independent subsidy calculator created by the Kaiser Family Foundation.

As of January 1st, there is Guaranteed Insurability for everyone. Carriers can no longer decline coverage to an individual based on previous or current medical issues. This is critically important for a lot of people. Carriers will have to allow you onto their plan regardless of your medical conditions. But there are open enrollments (discussed below) and one must apply by the 15th of the month prior to the effective date. If you want to have a plan on January 1st, you must apply for that plan (through the Exchange or directly with the carrier) by December 15th.

In order to help the carriers keep premiums low, Individual Coverage Mandates are implemented starting in 2014. That means everyone must have health insurance or pay a penalty. In 2014, that penalty is the greater of $95 or 1% of household income. In order to discourage people from going without insurance and just paying the penalty, the ACA only allows individuals to start health insurance at one time during the year.

This year, that’s January through April. In following years, it will be January 1st. If someone has a major medical issue, they may have to wait for several months until that issue is covered by health insurance. There is a lot more to the ACA, and we’re discovering more every day. Some of the detail may change, but here are some important issues that will not change.

Become more engaged in choosing a plan Make sure you understand your benefits. A broker can help you, and you won’t have to pay anything for their services.

Know that provider networks will be shrinking

Verify that providers who are critical to your care are on the plan before you apply.

Consider increasing your deductible

Most of the out-of-pocket maximums will be the same now. Health insurance is risk management. If your biggest risk is bankruptcy, and you can afford to pay the smaller bills yourself, maybe a higher deductible plan with a lower premium is a better fit for you.

Become a consumer of your care

Understand the costs. Check out websites like www.healthcarebluebook.com, where you can see what a procedure should cost in your area. Go directly to the labs to get work done. I’ve used www.healthcheckusa.com in the past and have been very happy with them. A quick Google search will show labs in your area. In both Oregon and Washington, there are free resources to get prescription discounts.